Solana 2025:

The Year of Internet Capital Markets

Introduction

Despite a broader market downturn, 2025 was a breakout year for Solana, driven not by speculation but by the compounding effect of years of infrastructure refinement and ecosystem expansion. Steady improvements in throughput, stability, fee markets, and client diversity have made Solana one of the most reliable execution layers in crypto. These upgrades, accumulated across multiple market cycles, created a technical foundation strong enough to support high-volume trading, instant settlement, and consistently low costs even as many other networks struggled.

At the same time, deliberate ecosystem growth has matured into a powerful economic engine. Stablecoin adoption has accelerated, tokenized real-world assets have expanded institutional activity, community launchpads have strengthened grassroots participation, and native multi-asset trading has flourished. The result of 2025 is a convergence of infrastructure and applications that is now driving real usage at scale. Solana’s long-term investments are paying off, turning the network into a resilient and fast-growing marketplace for internet-native finance despite challenging macro conditions.

Strategic partner

Key Takeaways

01.

Following an all-time high in SOL price in January, Solana generated $1.41 billion in real economic value (REV), ranking first among major blockchains for the first time and accounting for over one-third of total revenue across leading networks.

02.

Total DEX volume on Solana surpassed $3 trillion in 2025, exceeding BNB Chain by 1.2x, Ethereum by 3x, and Base by 5x, while growing 277% year over year compared to 2024. Over the same period, market leadership shifted from Raydium and Orca in 2024 to Meteora and Humidifi in 2025, highlighting rapid market evolution on Solana.

03.

Infrastructure-wise, Solana recorded zero outages in 2025, with average block time stabilizing at 0.398 seconds and variability in block metrics dropped more than 8x, from over 6–7% in 2024 to 0.83% in 2025. Performance improving updates such as Frankendancer, JitoBAM and DoubleZero saw rapid adoption across validators.

04.

Stablecoin supply grew from $5.2 billion to a peak of $16.8 billion (+220.6%), closing the year at $15.7 billion. Solana led all major chains in YoY stablecoin growth, averaging 282.9%, with a peak of 423.6% in January.

05.

Solana recorded the highest average monthly USDC turnover rate at 977.5%, meaning each USDC token was used more than 9 times per month, far exceeding BNB Chain (666.7%), Base (520.1%), and Ethereum (69.2%).

06.

Total RWA value on Solana reached $851.5 million with 123,396 holders, led by tokenized U.S. Treasuries (62.8%) and fast-growing tokenized equities, which surpassed $200 million in AUM and 50,000 holders within six months of launch. In parallel, Project Open led by Solana Policy Institute and Orca with support from other ecosystem partners is advancing regulatory frameworks for compliant on-chain securities.

07.

Bridged volume via Wormhole grew 258.3% YoY to $10.59 billion, while BTC-denominated assets on Solana reached a $1.88 billion market cap. Monad’s MON became the first L1 native token tradable on Solana from day one of mainnet, with first-day volume hitting $77.34 million.

08.

In 2025, Solana ranked first in new tradable token creation for 21 consecutive months, with over 40 million tokens created and Pump.fun capturing ~95% of launchpad volume and $870 million in cumulative revenue. Yet memecoin trading’s share of total volume went on a downward trend, signaling market maturation toward more sustainable and diversified forms of on-chain trading.

What Experts Say

Ecosystem Overview

Solana’s ecosystem reached a series of structural milestones in 2025. Following SOL’s rise to a new all-time high of $293.31 on January 19, on-chain activity across nearly every sector surged to record levels. By December 2025, Solana counted 4.81 million SOL holders, the largest native-token holder base among major blockchain networks. Holder growth accelerated meaningfully throughout the year, particularly in the second half of 2025, when the number of SOL holders doubled from roughly 2.4 million to 4.8 million within six months. Network activity closely tracked this expansion, with active and new addresses peaking at approximately 6.5 million during the January price high, and a 218% increase in domain registrations with Solana Name Services (SNS) throughout the year.

This surge in participation translated directly into economic output. Around the January peak, Solana recorded its highest network revenue at $56.82 million and its largest daily DEX volume at $43.26 billion. According to Blockworks, over the full year, Solana generated $1.41 billion in real economic value (REV), ranking first among major blockchains for the first year and accounting for more than one-third of total revenue across leading networks. Hyperliquid followed with $822 million, while Ethereum recorded $665.61 million.

Solana also led decentralized trading activity throughout 2025, with total DEX volume surpassing $3 trillion. This placed Solana ahead of other major networks, at approximately 1.2 times the volume of BNB Chain, nearly three times that of Ethereum, and five times Base. On a year-over-year basis, Solana’s DEX trading volume grew 277% compared to 2024, reflecting both rising user participation and a rapidly evolving exchange landscape.

Market structure on Solana evolved over the year. While Raydium and Orca dominated trading in 2024 with a combined 76.01% market share and maintained leadership into the first half of 2025 with 53.68% of total volume, the second half of 2025 saw the shift towards Meteora and the newly emerged prop AMM Humidifi. At peak, Humidifi captured 38.63% of total trade volume to become the leading DEX. This transition highlighted the ecosystem’s capacity for rapid market innovation and competition.

Beyond on-chain metrics, 2025 marked a turning point in Solana’s institutional and global presence. Flagship ecosystem events reached record attendance, including more than 3,000 participants and 20 policy makers at Accelerate NYC, and over 6,000 attendees and 200 speakers at Breakpoint Abu Dhabi. On October 30, Solana entered a new chapter by appearing directly on Wall Street with the launch of the Bitwise Solana Staking ETF (BSOL) and the ringing of the New York Stock Exchange closing bell. These moments symbolized a broader shift that unfolded throughout the year, with deeper institutional engagement positioning Solana as a credible foundation for internet-native capital markets.

In the sections that follow, this report examines how maturing infrastructure powers the core pillars underpinning Solana’s emergence as an internet capital market in 2025, including stablecoins, native crypto assets, real-world assets, and launchpads.

Infrastructure: Increasing Bandwidth

and Reducing Latency

Once defined by instability, Solana has spent recent years executing on a clear infrastructure mandate focused on increasing bandwidth and reducing latency (IBRL). Since 2023, the network has experienced only two major outages and two periods of degraded performance, with no outages recorded in 2025. Even during periods of extreme activity, including January’s price-driven congestion and October’s mass liquidation event, the network continued to operate smoothly.

Network-level metrics in 2025 further reflect this maturation. Daily block production and average block time stabilized around 217,300 blocks per day and 0.398 seconds, respectively, marking a significant improvement over prior periods. This stabilization began in February 2025, following a year characterized by greater variability. From January 2024 through January 2025, Solana’s coefficient of variation stood at 6.84% for block count and 7.14% for block time. From February through December 2025, variability fell sharply to 0.83% for both metrics, more than an eightfold reduction. Even at its highest, average block time reached just 0.4066 seconds, only 1.65% above the network’s 0.4-second target, underscoring the consistency and reliability achieved over the year.

Despite this, teams continued to push performance boundaries through validator update releases. In October 2025, the Agave client released version 3.0, delivering 30-40% faster transaction processing, 40% higher compute limits, and significantly reduced startup times compared to earlier versions. In parallel, Jump Crypto’s Firedancer client continued to demonstrate performance gains through its Frankendancer implementation. By October 2025, Frankendancer validators processed 12.8% more non-vote transactions per block, packed blocks more efficiently with 7.5% more CUs, and earned 5.9% higher priority fees than Agave-based validators, excluding version 3.0. One validator even briefly exceeded 100,000 TPS in production conditions. Adoption accelerated steadily throughout the year, growing from just 6 validators representing 0.78% of total stake to a peak of 214 validators accounting for 25.98% of network stake by November.

In July, Solana Labs, Anza, DoubleZero and other core infrastructure teams jointly released The Internet Capital Markets Roadmap, outlining a coordinated strategy to make Solana infrastructure-ready for large-scale, high-performance financial markets. The roadmap identified key priorities across networking, block production, and consensus, with the explicit goal of pushing throughput and latency beyond the limits of conventional blockchain architectures. Since its publication, multiple initiatives highlighted in the roadmap have moved rapidly into production or advanced testing, delivering measurable performance gains.

Several of these upgrades are already live on mainnet. BAM and DoubleZero have been deployed, while Alpenglow has entered private testnet. BAM, or Blockspace Assembly Markets, introduces a next-generation transaction scheduling framework that decouples transaction ordering from validation. This architecture enables ecosystem developers to build financial primitives such as central limit order books, perpetual exchanges, and dark pools that require deterministic sequencing and privacy guarantees. Since going live in November, Agave JitoBAM has seen rapid adoption, with validator participation exceeding 200 within the first week of January 2026 and peak stake reaching 12.5%.

DoubleZero complements these advances at the physical networking layer, representing the internet in Internet Capital Markets. As a purpose-built, high-performance fiber network for distributed systems, DoubleZero is designed to unlock throughput and latency levels unattainable on the public internet. Following its mainnet launch on October 2, 2025, DoubleZero reduced median skip rates by an order of magnitude, from 0.39% to 0.04%, while median earned credits increased from 99.53% to 99.55%. Adoption has been swift, with 396 validators integrating the DoubleZero stack within three months, representing 39.01% of total network stake.

Looking ahead, Alpenglow represents the next frontier in Solana’s consensus evolution. Targeted for mainnet deployment in 2026, Alpenglow has already demonstrated 150-millisecond finality on a 50-node globally distributed cluster, representing a 266% reduction relative to Solana’s current 400-milisecond target block time. Together, these infrastructure advances establish the technical foundation required for high-frequency settlement, deep liquidity, and real-time capital movement.

Stablecoins: The Liquidity Engine

In 2025, Solana emerged as the fastest-growing major stablecoin ecosystem, turning stable assets into one of its most powerful economic drivers. While Solana ranked third in absolute stablecoin supply behind Ethereum and Tron, it led the industry in growth velocity. Total stablecoin supply expanded from $5.2 billion to a peak of $16.8 billion on December 12, representing a 220.6% increase, before closing the year at $15.7 billion. Throughout 2025, Solana consistently posted the highest year-over-year growth rates among major networks, averaging 282.87% and reaching a peak of 423.59% in January, driven by a net inflow of $6.15 billion in stablecoin supply. Month-over-month and quarter-over-quarter growth also ranked first, highlighting sustained rather than episodic adoption.

USDC continued to dominate Solana’s stablecoin landscape, reinforcing the network’s role as a preferred settlement layer. By December 21, USDC supply reached $10.4 billion, accounting for 66.24% of total stablecoin supply on Solana. This figure stood nearly five times higher than USDT at $2.1 billion and roughly eight times larger than PYUSD at $1.1 billion. Notably, Solana ranked second globally in USDC supply for 13 consecutive months through December 2025, surpassing Base and Arbitrum since November 2024 and signaling sustained issuer and user preference for Solana-based settlement.

High supply translated directly into high utilization. USDC trading volume on Solana consistently exceeded that of USDT, with a daily mean volume of $1.79 billion and a median of $6.71 billion. Activity peaked during periods of market stress and volatility, including SOL’s January all-time high and the October 10 liquidation event, demonstrating Solana’s capacity to absorb large-scale capital flows.

Utilization efficiency further set Solana apart. From January 2024 through December 2025, Solana recorded the highest average monthly USDC turnover rate at 977.48%, meaning each USDC token was used more than nine times per month for trading. By comparison, BNB Chain recorded 666.71% and Base 520.13%, while Ethereum, despite its larger absolute supply, posted a much lower turnover rate of 69.21%.

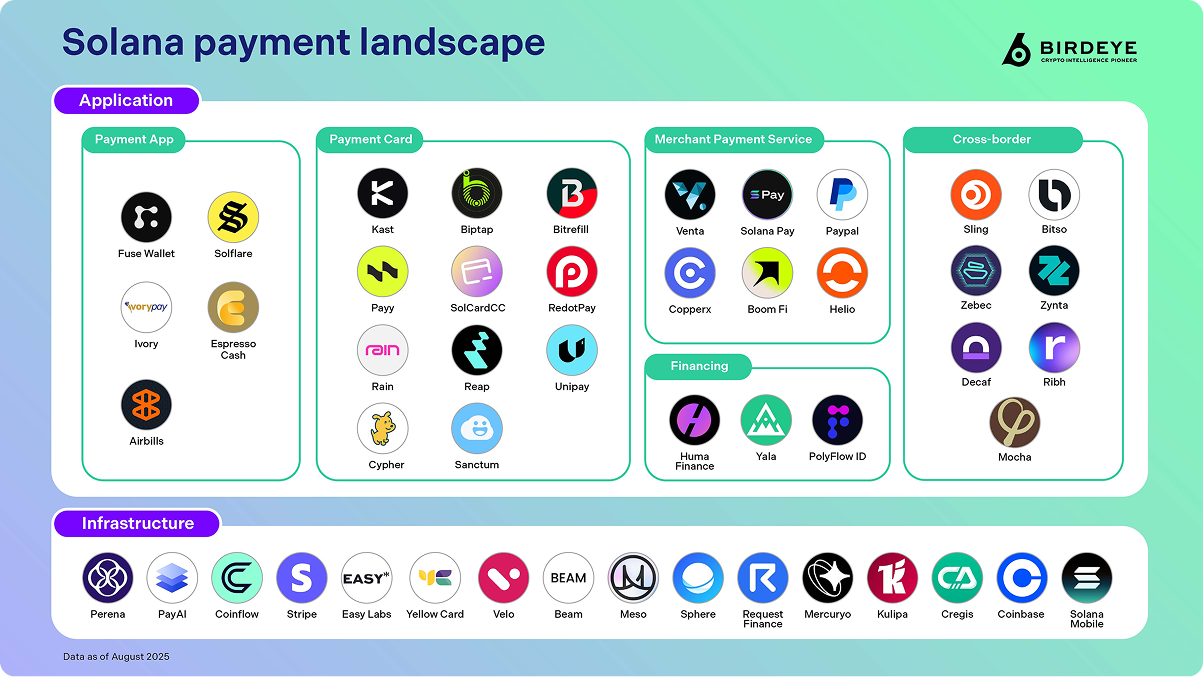

Beyond trading, stablecoins on Solana are increasingly expanding from DeFi infrastructure into mainstream payment and settlement use cases. This shift is particularly pronounced on Solana due to its low fees, fast finality, and user experience that closely resembles Web2 systems. By August 2025, the ecosystem supported 26 payment-focused applications and 14 infrastructure projects, with 40% of these operating exclusively on Solana, reflecting growing specialization around stablecoin-based payments.

Institutional adoption further reinforced this trend. On December 16, Visa launched stablecoin settlement in the United States on Solana, enabling 7-day-per-week settlement for its initial banking partners, Cross River Bank and Lead Bank. This marked a significant milestone for stablecoin integration into traditional financial workflows and underscored Solana’s emergence as a viable settlement layer for regulated, real-world payment systems.

Real-World Assets: Solana’s Bridge to

Traditional Finance

By December 2025, Solana had established itself as one of the leading networks for real-world asset tokenization, ranking third by both distributed RWA value and holder count. Total RWA value on Solana reached $851.5 million, supported by 123,396 unique holders. Tokenized U.S. Treasuries represented the largest share at 62.8% of total RWA value, reflecting strong demand for on-chain, yield-bearing instruments.

BlackRock’s BUIDL led the category with $255.21 million in distributed value, followed by Ondo Finance’s USDY and OUSG at $175.67 million and $71.03 million respectively. While BUIDL and OUSG remain permissioned products restricted to institutions and verified purchasers, USDY operates as a yield-bearing stablecoin accessible to retail users, offering APYs ranging from 3.62% to 5.1%. By the end of 2025, USDY had attracted more than 7,000 holders on Solana.

Tokenized equities emerged as the second-largest RWA category on Solana, accounting for 22.5% of total RWA value. This segment was dominated by tokenized public equities, which represented 21.7%, while private equities accounted for a smaller 0.8%. Public equity tokens issued through platforms such as xStocks and rStocks were the fastest-growing RWA sector on the network. Since launching in July, tokenized equities surpassed $200 million in assets under management and reached over 50,000 unique holders by December 2025. Among these, Tesla xStock (TSLAx) led with $49.15 million in AUM, more than double Circle xStock (CRCLx) at $21.80 million and Nvidia xStock (NVDAx) at $18.77 million.

Unlike institution-only instruments like BUIDL and OUSG mentioned above, tokenized equities on Solana are permissionless and fully composable within DeFi. They trade continuously on-chain, are available 24/7, and can be integrated into lending, trading, and structured products. In 2025, tokenized stocks generated $512.95 million in DEX trading volume, with xStocks products accounting for 80.64% of total volume. Despite their round-the-clock availability, trading behavior closely resembled traditional markets, with weekend volumes averaging 61.41% lower than weekday activity.

From a cross-chain perspective, Solana’s tokenized public equity value reached approximately 52% of Ethereum’s $354-million market, where Ondo Finance accounted for $227.94 million in tokenized stocks and ETFs. With Ondo Global Markets planning to expand to Solana in Q1 2026, the network is positioned to capture a larger share of tokenized equity issuance and trading.

On the policy front, Project Open, a joint initiative led by the Solana Policy Institute and Orca alongside other ecosystem partners such as Phantom, and Superstate, has been actively engaging with the U.S. Securities and Exchange Commission to propose regulatory frameworks that enable compliant blockchain-based issuance and trading of securities. Together, expanding issuer participation and proactive policy coordination are expected to accelerate Solana’s RWA growth and further establish real-world assets as a core pillar of its internet capital markets in 2026.

Beyond treasuries and equities, tokenized commodities on Solana began to gain traction in the second half of 2025, albeit from a smaller base. Paxos’s tokenized gold product, PAXG, led this category as monthly trading volume increased nearly tenfold from $26,318 in July to a peak of $244,959 in November. Over the same period, the number of holders rose from 60 to 686. While still modest compared to Ethereum, this acceleration points to growing interest in on-chain commodity exposure and highlights the potential for further RWA diversification as Solana’s liquidity and institutional participation continue to expand.

Native Crypto Markets: Solana as the

Home of Multi-Asset Trading

In 2025, Solana experienced record inflows from cross-chain bridges, reinforcing its role as a destination for liquidity and multi-asset trading. Total bridged volume to Solana increased significantly year over year, driven primarily by Ethereum-based assets. Via Wormhole, bridge volume grew 258.29% from $4.1 billion in 2024 to $10.59 billion in 2025, with Ethereum’s share of inflows rising from 76.5% to 83.08%.

deBridge also recorded strong growth, with bridged volume to Solana increasing 158.78% from $1.94 million to $3.06 million. While Ethereum remained the largest source of capital, its share of deBridge inflows declined from 58.48% to 41.41%, as inflows from BNB Chain expanded rapidly, increasing 517.47% from $1.02 million to $5.26 million. These trends point to a broader diversification of capital sources entering the Solana ecosystem.

Bridged assets, together with natively deployed tokens from other layer-1 networks, have become a major component of Solana’s on-chain asset mix. The most notable shift occurred in the BTC token market. Following the introduction of Coinbase’s cbBTC in late 2024 and the expansion of WBTC bridged via Wormhole, BTC-denominated assets rapidly overtook WETH in market capitalization on Solana. From a low point of 65.28% relative to WETH at the start of 2024, BTC token market capitalization climbed to a peak of 697.14% of WETH by December 7, 2025. Total BTC token market cap reached $1.88 billion on October 6, coinciding with Bitcoin’s all-time high.

A closer examination of BTC tokens highlights the pace of this shift. Between 2024 and 2025, WBTC bridged via Wormhole expanded its supply more than thirteenfold, rising from 301.97 tokens in January 2024 to a peak of 4,069.31 tokens on November 21, 2025. Despite entering the market later, cbBTC exhibited even faster adoption, reaching a peak supply of 4,646.36 tokens on October 7 and surpassing WBTC to become the largest BTC token on Solana by supply. In the second half of 2025, cbBTC also led in trading activity, recording average daily volumes 74.17% higher than WBTC as holder counts converged. At current growth rates, cbBTC is on track to surpass WBTC in holder count in the first quarter of 2026.

Beyond Bitcoin and Ethereum assets, 2025 also marked a turning point for native layer-1 tokens deploying directly on Solana. Tokens such as Tron’s TRX, Zcash’s ZEC, Hyperliquid’s HYPE, and Monad’s MON became tradable within Solana’s ecosystem. By year-end, ZEC recorded the highest market capitalization among these assets at $28.24 million, alongside the largest cumulative trading volume at $1.32 billion. While its market cap and total volume were smaller, Monad’s MON stood out due to a sharp trading surge at launch, reaching $77.34 million in volume on November 25. MON’s deployment represented the first instance of a layer-1 native token being available for trading on Solana from the first day of its mainnet launch, highlighting Solana’s growing role as a neutral, high-performance venue for cross-ecosystem asset trading.

Launchpads: Community

Capital Formation

Following the market dislocation in 2023 triggered by the FTX collapse, Solana’s on-chain activity began to recover in 2024, led by a resurgence in retail trading and the rise of memecoin-driven speculation. Early successes such as BONK and dogwifhat set the stage, but the launch of Pump.fun marked a fundamental shift in how tokens were created and distributed. For the first time, launching a memecoin required virtually no capital or technical expertise. With minimal cost and no coding skills, users could deploy tokens that were immediately tradable and liquid on a bonding curve. This innovation dramatically lowered barriers to participation and repositioned launchpads as a central mechanism for community-led capital formation.

Pump.fun’s impact quickly reshaped Solana’s market structure. As the platform gained traction, Solana became widely recognized as the leading memecoin ecosystem. The network ranked first in new tradable token creation for 21 consecutive months starting in April 2024. Activity peaked in January 2025, coinciding with the launch of $TRUMP on Solana, when more than 1.6 million new tokens were traded in a single month. Pump.fun accounted for 97% of this activity, underscoring its dominance as the primary launch venue during the height of the memecoin cycle. While Pump.fun continued to lead daily token deployments throughout the year, July marked a brief exception when LetsBonk overtook the platform. On July 21, LetsBonk recorded 28,872 tokens deployed in a single day, more than three times Pump.fun’s output and representing 67.55% of total daily deployments.

Pump.fun’s dominance extended to volume and revenue. By the end of December 2025, Pump.fun captured approximately 95% of launchpad trading volume and revenue on Solana, with cumulative revenue reaching $870 million according to DefiLlama. Average monthly trading volume grew 42.5% year over year, rising from $32.12 million in 2024 to $45.77 million in 2025. Despite the scale of token creation, market activity remained highly concentrated. The top ten tokens by market capitalization represented more than 55% of total token market cap, even as the total number of tokens created surpassed 40 million.

By 2025, however, the composition of trading activity on Solana began to shift. While memecoins led volume in 2024, accounting for an average of 49.27% of all trading, their share declined sharply to approximately 14.98% in 2025. In parallel, activity in SOL pairs, stablecoin swaps, and other DEX markets increased, overtaking memecoin trading. This transition signals a broader maturation of Solana’s capital markets, as the ecosystem moves beyond peak speculative cycles toward more sustainable and diversified forms of on-chain trading.

Conclusion

Solana’s performance in 2025 illustrates the power of long-term compounding in both infrastructure and ecosystem design. Years of focused investment in bandwidth, latency reduction, client diversity, and reliability converged at a moment when real demand arrived. Rather than relying on short-lived narratives, Solana entered 2025 with a production-ready execution layer capable of supporting high-frequency trading, institutional settlement, and consumer-scale payments, even as broader crypto markets faced macro headwinds.

What distinguishes this phase of growth is the breadth and depth of activity now occurring on the network. Stablecoins have become a core liquidity and payment rail, real-world assets are bridging on-chain markets with traditional finance, launchpads continue to democratize capital formation, and native crypto markets are expanding Solana’s role as a neutral venue for trading assets from across the crypto landscape. These pillars reinforce one another, creating a feedback loop where infrastructure enables usage, usage attracts liquidity, and liquidity justifies further institutional and developer commitment.

Special thanks

We would like to express our sincere gratitude to partners and friends

who have supported us and provided data so that we can complete this report.